Subscribe to Our Newsletter

Hear more from Equity Methods: Your trusted partner in equity compensation excellence.

Should stock-based compensation (SBC) be excluded from non-GAAP earnings? To some, it’s one of the biggest debates about the presentation of financial results, while to others, it’s as obvious as the sky is blue. But what’s obvious today is controversial tomorrow, making this a relevant question to any public company CFO and CAO.

Critics call the exclusion of SBC obfuscation. Defenders say it’s a sensible adjustment that helps investors see through the noise of a non-cash charge. As for us (spoiler alert), we’re not taking a side. We’re more interested in what kind of companies exclude SBC and when they decide to start including it.

For insight, we reviewed the most recent earnings release for every company in the S&P 500 and classified each one by whether SBC appears as a reconciling item in their GAAP to non-GAAP bridge. We then cross-referenced those classifications against sector, revenue size, SBC intensity, and revenue growth.

What emerged was a set of observable patterns indicating when the case for excluding SBC may begin to weaken. These, paired with an understanding of investor expectations and behaviors, can give CFOs and CAOs a more rigorous way to determine when it may be time to transition from exclusion to inclusion. Just as importantly, they provide a useful yardstick for assessing shifts in investor sentiment regardless of the company’s own presentation choice.

Before turning to those thresholds and their implications, it’s worth exploring some of the arguments for and against excluding SBC from non-GAAP earnings.

Stock-based compensation is, from a generally accepted accounting principles (GAAP) standpoint, unambiguously an expense. But accounting and economics are two different things. SBC is a prime example of how accounting classifications don’t always reflect how investors think about valuation.

For high-growth companies, SBC functions more like a capital investment than a recurring operating cost. It also has a binary quality that mature-company frameworks tend to miss: Either the growth company hits its business plan—in which case the SBC cost and dilution will look very different in the firm’s future financials—or it doesn’t, and there won’t be much to say.

In higher-growth contexts, excluding SBC from non-GAAP earnings can have a clarifying effect. Investors are better served by seeing the cash-generative economics of the business without a non-cash charge whose long-run significance is genuinely unresolved.[1]

Problems arise when companies stay in exclusion mode longer than the underlying facts support. Two dynamics are worth monitoring.

Narrative Drift

Narrative drift occurs when there’s a wide gap between what investors actually do and the story the financials are trying to tell.

Remember, presentation is the company’s choice while valuation is the investor’s. As a company matures into more predictable growth, SBC starts looking like what it is: a recurring cost of doing business. At that point, investors adjust their approach to valuation, often by applying a haircut to non-GAAP presentations that exclude SBC and other clearly recurring costs of doing business.

A related consideration is that investor behavior also changes if SBC begins growing faster than revenue. At this stage, the “non-cash, non-recurring” framing loses credibility. SBC no longer looks like a modest capital investment in pursuit of outsized future growth. Investors may tolerate super-sized SBC early on because they expect future revenue growth to more than offset today’s dilution and expense burden. If conviction in that growth case weakens, investors become more likely to build SBC cost and dilution directly into their valuation assessments.

Financial reporting is the company’s opportunity to explain what has happened and what lies ahead. To be effective, the story must remain tethered to where the organization stands in its growth lifecycle.

Ultimately, this comes down to a broader question about the role of financial statements. Should they present information in line with how the “typical” investor is already approaching valuation, or should they present information in the way management believes information should be used?

To be clear, we don’t think there’s anything manipulative about the latter. Investors are well-equipped to interpret financial statements however they so choose, including GAAP to non-GAAP bridges. Obviously, there isn’t even such a thing as the “typical” investor: the entire reason markets work is that investors disagree and the price mechanism is how winners and losers are written into history. That’s why we see this as a philosophical decision, one that the CFO, CAO, CEO, and audit committee should make in light of investor feedback.

Internal Forecasting Neglect

SBC often gets less managerial and forecasting attention when it sits outside the non-GAAP metric. That’s a problem because SBC is a high-risk audit area, and cost surprises do affect valuation for the reasons noted above. While this risk is entirely manageable, experience suggests it increases when SBC is persistently excluded from non-GAAP earnings presentations.

Whether it’s excluded from non-GAAP earnings or not, SBC should get increasingly more attention and control as an organization matures. The cost and challenge of repairing a fragmented, sprawling SBC process far exceeds what it takes to implement a streamlined and integrated process before complexity takes hold.

So what prompts companies to start including SBC in non-GAAP earnings? We find that common triggers are maturity, SBC granting intensity, and revenue growth.

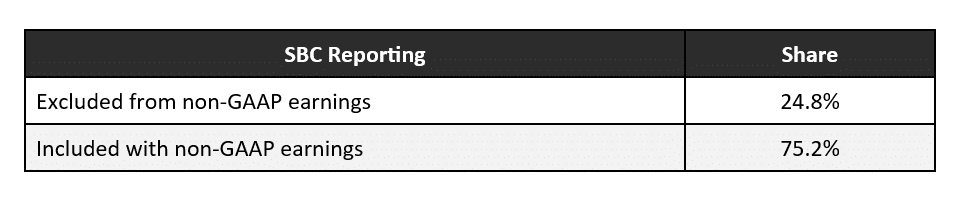

One threshold is maturity. Overall, most S&P 500 companies include SBC with their non-GAAP earnings. Only about 25% don’t.

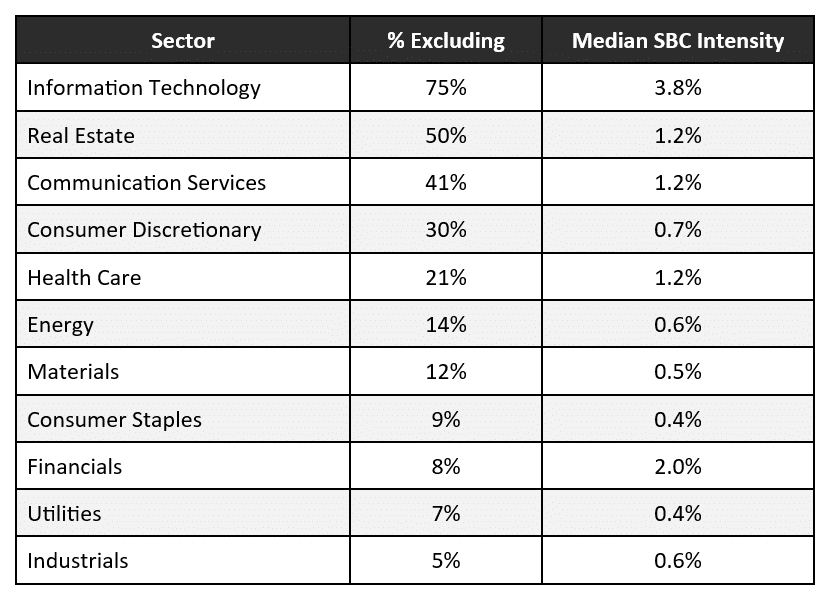

But among technology companies within the S&P 500, it’s the other way around, with 75% of them excluding SBC. The tech sector is unique in part because of its median SBC intensity, or SBC expense as a percentage of revenue or operating income. SBC intensity reflects the magnitude of equity compensation relative to the scale of the business. At 3.8% of revenue, it’s roughly three to five times higher in tech than in most other sectors.

By comparison, only 5% of industrials and 8% of financials exclude SBC. These are not sectors with insignificant equity compensation programs. However, they carry much lower SBC-to-revenue ratios. And in financials, the distinction between SBC and other compensation structures is often less clean.

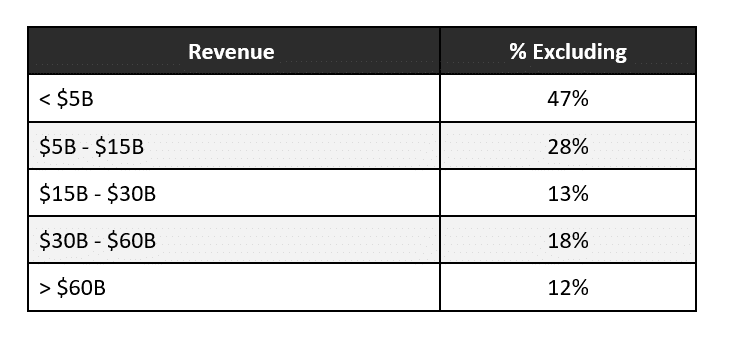

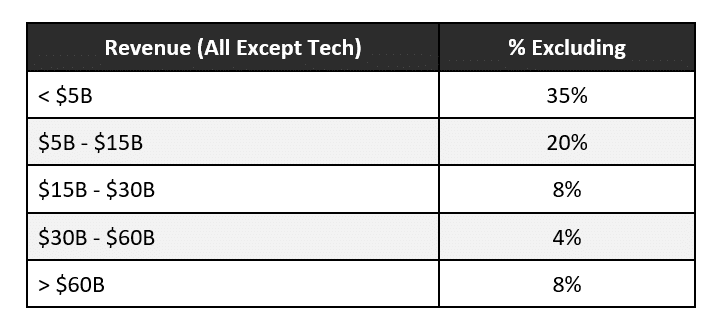

Revenue is better than industry sector at indicating company maturity because it more closely tracks the underlying economic rationale for including or excluding SBC. Below $5 billion in revenue, nearly half of companies exclude SBC. Above $15 billion, that rate drops into the low teens.

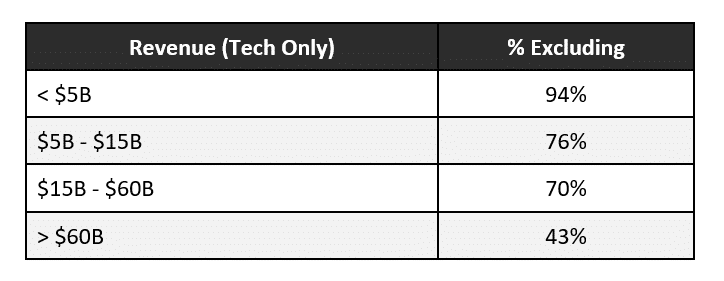

Still, technology is an outlier, even when controlled for revenue. The share of tech companies that excludes SBC doesn’t fall significantly until revenue exceeds $60 billion.

By contrast, there’s less tolerance for other high-revenue companies to exclude SBC, as shown when we omit tech from the analysis.

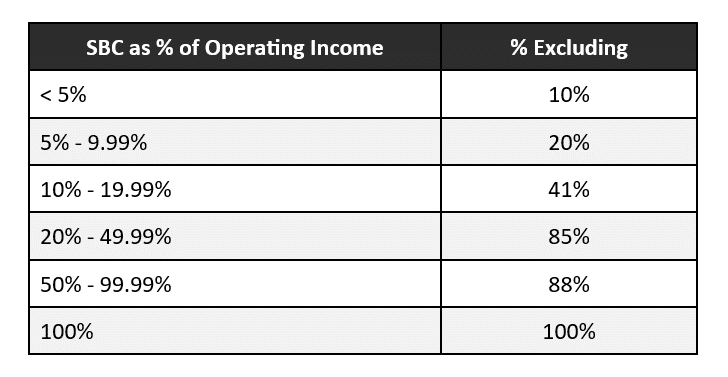

SBC intensity is a reliable predictor of exclusion, whether expressed as a percentage of revenue or as a percentage of operating income.

Consider operating income first. As the following table shows, the share of companies that exclude SBC plunges once SBC drops below 20% of operating income. While many companies delay making the transition, 20% serves as a reasonable bellwether of organizational maturity.

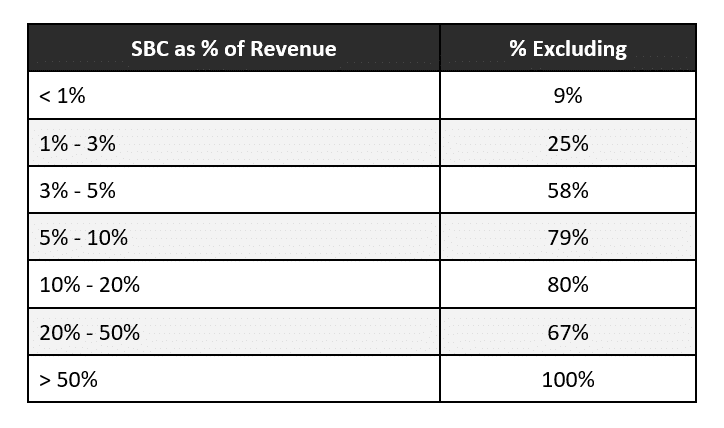

An analysis of SBC as a percentage of revenue also reveals a step change. Below 1% of revenue, nearly all companies include SBC. Above 5%, most companies exclude it.[2]

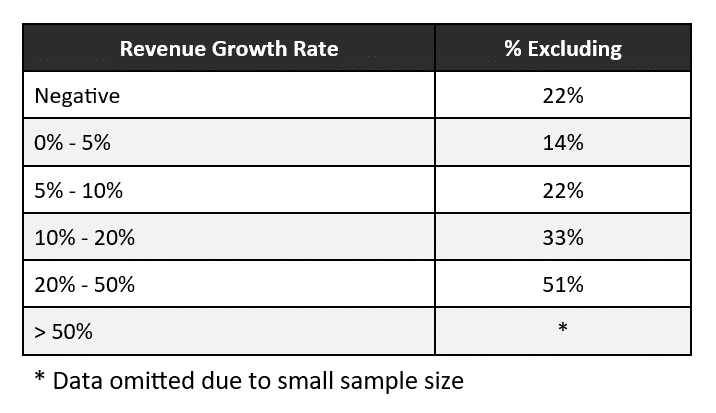

The greater the rate of revenue growth, the more likely companies are to exclude SBC, as the following table shows.

1. There’s no single right answer, but there is a lifecycle.

The data shows that earlier-stage, faster-growing, SBC-intensive companies tend to exclude SBC. That’s consistent with the underlying observation that, early on, SBC is more akin to an investment and becomes a rounding error if the expected growth materializes. The market broadly accepts this.

As companies progress along the revenue and organizational maturity curve, the question becomes whether that exclusion has overstayed its welcome. At some point, investors will begin to view the non-GAAP presentation as introducing friction and opacity rather than telling a simpler, cleaner story.

2. Revenue scale is a better trigger than market cap.

Market cap is a much noisier metric than revenue. Exclusion rates range from 22% to 43% across market cap categories, with no directional trend.

Why? Because market cap reflects sentiment and future expectations for growth, whereas revenue tracks the actual scale of the operating business. For boards thinking about when to revisit their exclusion policy, revenue milestones are the more reliable trigger points.

At a broad market level, revenue above $5 billion appears to mark the point at which excluding SBC is no longer common practice, a pattern that generally holds outside the technology sector. If the CFO and board are looking for a natural checkpoint at which to revisit the policy, revenue milestones are a reasonable anchor.

Within tech, exclusion remains above 50% until revenue hits $60 billion, so there’s ample air cover. Nonetheless, a notable minority (around 25%) of companies with $5 billion to $60 billion in revenue do include SBC. These skew toward hardware and semiconductor firms, where SBC levels are structurally lower than in software. Even so, there’s still a conversation to be had on timing and market signaling.

Our advice is to begin modeling and presenting SBC-inclusive results internally well before reaching your intended transition threshold. Suppose the goal is to include SBC once doing so would no longer turn positive non-GAAP earnings negative. In that event, we’d suggest modeling SBC-inclusive results at least two years in advance. This allows internal stakeholders to adjust and gives processes time to mature accordingly.

3. SBC intensity predicts the choice and the scrutiny.

When SBC exceeds 20% of operating income or 5% of revenue, the prevalence of exclusion exceeds 75%. That’s not surprising. Where things get interesting is when SBC becomes the switch that flips profit to loss. This is also when investors and proxy advisors begin paying closer attention to the GAAP-versus-non-GAAP divide, and when SBC emerges as a critical audit matter or an area of significant testing.

The most effective CAOs and CFOs in this group are transparent about excluding SBC, but back that decision with a world-class reporting process. The risk lies in treating SBC as irrelevant or overlooking it altogether, which is precisely when critical audit matters can turn into material weaknesses.

4. Transparency into SBC is coming for everyone, not just excluders.

Much of the exclude-versus-include debate assumes companies will continue to present compensation costs the way they do today. That assumption has a limited shelf life. ASU 2024-03, the FASB’s income statement disaggregation standard, is effective for fiscal years beginning after December 15, 2026. It will require companies to disaggregate functional expense lines (COGS, SG&A, and R&D) by the nature of the expense. Employee compensation is one of the five required natural categories.

The practical effect is that the “black box” within each functional line begins to open up. For the first time, analysts on earnings calls will be able to ask why R&D employee compensation grew 18% while revenue increased only 6%. This added granularity will lead to considerably more investor inquiry, and in turn, require upgrades across the SBC reporting and analytics process.

5. Whether or not you exclude, SBC demands rigorous forecasting.

According to our research, SBC is growing faster than revenue at roughly half of S&P 500 companies. To our surprise, this is roughly equally true among excluders and includers. When SBC is growing faster than revenue, it automatically becomes an area of investor focus. Even when it’s not, there are still warning signs to watch for, such as a revenue slowdown that could upset the apple cart.

This means SBC is a real and growing cost that requires proactive management, regardless of its treatment in the non-GAAP reconciliation. We’ve written and spoken extensively on what “good” looks like in SBC forecasting, planning, and analytics, including in our recently published SBC Best Practices Survey.

Excluders arguably face greater risk from weak forecasting. When SBC sits outside the non-GAAP metric, it can receive less analytical attention. But as noted earlier, presentation doesn’t dictate valuation—investors will assess SBC as they see fit, regardless of the corporate decision to exclude it. Que sera, sera, as the next point illustrates.

6. Investors start pricing in SBC before companies stop excluding it.

The transition from “excludes” to “includes” is obviously a company decision. But in practice, investors are making their own adjustments long before a company changes its presentation. At very early stages, loosely defined as under $1 billion in revenue, SBC is inherently irrelevant to how investors value the business. The business is closer to a lottery ticket that either will or won’t pay off in the form of a scalable, durable business model. In that context, the current cost structure is beside the point.

As the business matures and its economics become clearer, investors begin incorporating SBC into their own models, and this decision is independent of how it’s treated in the company’s headline non-GAAP number. They apply their own valuation multiples, adjust discounted cash flow and cost-of-capital assumptions, and make their own decisions about add-backs and exclusions based on their assessment of the company and its industry. (This is the “que sera, sera” point.) We’ve covered this dynamic extensively in other research, this being one example.

As a result, by the time a company switches its presentation format, most investors have already been working with SBC-inclusive numbers for some time. The formal transition to inclusion is simply a recognition of how the market is already evaluating the business. Framed this way, the decision becomes less about optics and more about understanding how investors are using the reported information.

7. The switch from “excludes” to “includes” is a high-stakes moment. Plan for it early.

When a company stops excluding SBC, it faces a one-time reset in its reported non-GAAP numbers. If SBC is 10% of revenue, that’s not a rounding error. The transition should be planned well in advance, not triggered by investor pressure.

Nvidia’s approach offers a useful model. The company announced the change one full quarter in advance, quantified the impact (a $1.9 billion hit to non-GAAP operating expenses and a 0.1% effect on gross margin), and framed it as a reflection of organizational maturity. Investors received a clear picture of what was changing and why, well before it showed up in results.

Getting to that position requires multi-year monitoring of SBC as a percentage of revenue and operating income, along with governance structures that flag when trends are moving toward an eventual transition. Nvidia is, of course, an exceptional case given its ~3,000% stock price growth from 2019 to 2026. So while instructive, it’s not the easiest to generalize.

8. The SEC’s concern is rarely the exclusion itself. It’s how you present it.

The SEC’s scrutiny of non-GAAP metrics has been on a clear upward trajectory, with a steady increase in comment letters related to non-GAAP disclosures. The risk is arguably lower today in light of the SEC’s numerous Corporation Finance Interpretations[3] and public comment letters. Still, it’s important to keep a close eye on the quality and clarity of these disclosures.

9. No matter what, transparency wins the day.

For many companies, the case for excluding SBC from non-GAAP earnings presentations is strong. But exclusion should never come at the expense of transparency.

That’s when the SEC takes notice, and when investor friction begins to create costs in the form of valuation discounting. Instead, prominently disclose GAAP earnings, provide a clean and understandable reconciliation, and discuss SBC trends in the MD&A. Investors who want the non-GAAP view can access it. Those who want to make their own adjustments have what they need.

Ultimately, the question investors are asking isn’t whether SBC is excluded (it takes a freshman-level introductory accounting course to figure that out). It’s whether the financials are high-quality, clear, and decision useful. That signaling effect has far more influence on valuation and the development of long-run investor cohorts.

Some have framed the SBC exclusion debate as a question of integrity. We think it’s better understood as a question of fit: fit with the company’s maturity, fit with investor expectations, and fit with the quality of the underlying reporting process.

The data shows that exclusion is concentrated right where you’d expect it: high-growth, SBC-intensive companies, especially in technology. But lifecycle progression is relentless. Revenue grows, growth rates moderate, and suddenly there’s a new signal of organizational maturity to convey.

As our data shows, there isn’t a single trigger point, but there are markers. And while there’s more air cover to delay in tech than in other sectors, that flexibility isn’t indefinite.

Our conclusion isn’t that excluding SBC is inherently problematic. Instead, it’s that SBC matters to investors, and presentation choices don’t have a mystical ability to dissuade them from incorporating it into valuation. As companies mature, investors begin pricing in SBC, often long before management officially includes it in non-GAAP results.

By the time inclusion feels right, investors have typically been pricing SBC into valuation for quite some time. This is why we advocate for world-class SBC processes regardless of presentation. The uptick in focus and inquiry linked to ASU 2024-03 will only amplify this expectation.

Our research also underscores the importance of planning the transition to inclusion well in advance. Nvidia’s clear announcement with a quantification of the impact, which it framed as a sign of organizational maturity, provides a timely and instructive example.

SBC is too large and growing too fast at too many S&P 500 companies to be managed passively. Companies that treat it as a governance priority are better positioned to earn investor confidence, withstand regulatory scrutiny, and maintain internal planning discipline.

We reviewed the most recent Item 2.02 Form 8-K (earnings release) for every S&P 500 company as of early 2026, 472 companies in total after excluding dual-class duplicates and two companies that exited the index. For each, we determined whether SBC appeared as a named line item in the GAAP to non-GAAP reconciliation.

Companies were classified as “Excludes SBC” if SBC appeared as a reconciling item (e.g., in a bridge from GAAP EPS to non-GAAP EPS, or from GAAP operating income to Adjusted EBITDA). All others were classified as “Includes SBC.” This category includes both companies that present non-GAAP measures without excluding SBC and companies that report solely on a GAAP basis.

We applied a rigorous set of quality controls to avoid common misclassification errors, including the cash flow statement add-back under ASC 230, antidilutive share adjustments under ASC 260, and excess tax benefit commentary that refers to SBC without excluding the expense. We also conducted an independent replication.

Financial data was sourced from S&P Capital IQ as of December 31, 2025.

****************************************************

[1] To illustrate this point more starkly, imagine a newly public technology company with $200 million in revenue and $800 million in costs, of which $300 million is attributable to SBC. The firm’s market cap is $2 billion. The investor’s calculus is almost entirely binary: Either the company executes on its business plan, in which case the revenue base will be multiples of where it is today and the $300 million in SBC has little bearing on the future economics; or it doesn’t, in which case enterprise value collapses and the SBC figure becomes moot for an entirely different reason. In neither scenario does today’s $300 million meaningfully inform what the business is worth.

[2] Remember, we’re only talking about presentation. A rule of thumb among technology CFOs is that SBC exceeding 20% of revenue enters an “orange zone” where investors begin to question whether future growth will adequately offset dilution.

[3] In case you missed it, in March 2026, the SEC renamed its Compliance and Disclosure Interpretations (C&DIs) to Corporation Finance Interpretations (CFIs). This puts an end to a long-debated question of whether the correct acronym was C&DIs, CDIs, or CD&Is. For the record, we were strongly and proudly in the first camp.