Subscribe to Our Newsletter

Hear more from Equity Methods: Your trusted partner in equity compensation excellence.

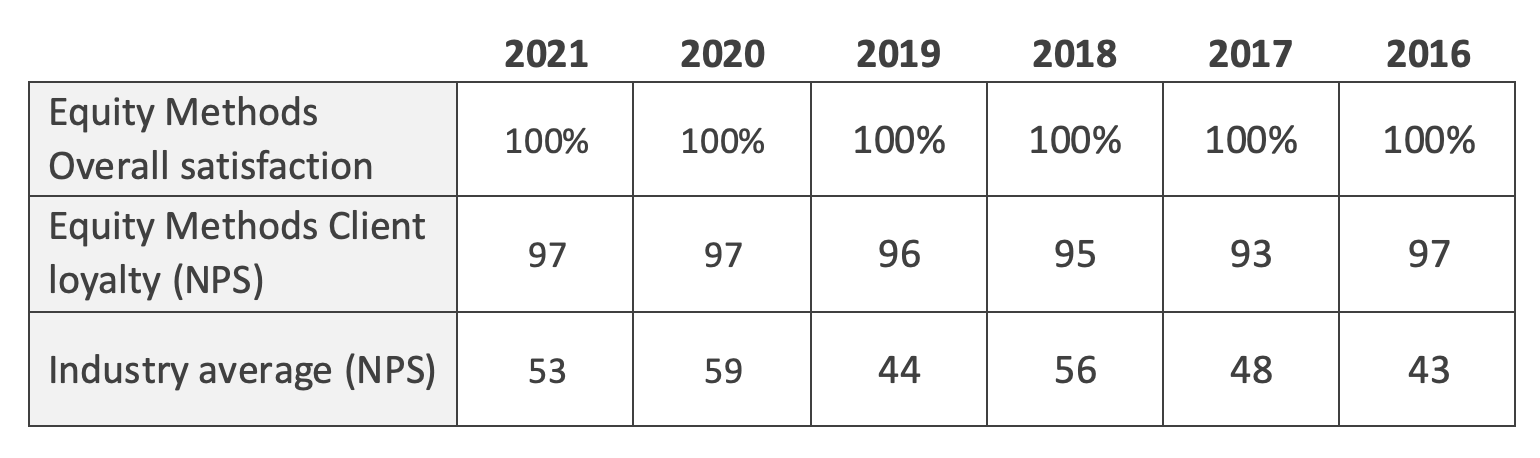

Every fall, Group Five publishes their annual stock-based compensation administration and financial reporting study. We participate in the latter and, for the eighth consecutive year, were the top-rated financial reporting service provider.

We flashed the high-level results in October. So I’ll offer some additional detail, then use the majority of this post to focus on a few equity compensation financial reporting themes we’re expecting to see in 2022:

Theme 1: Continuation of the shift toward relative performance metrics

Theme 2: Forecasting in response to uncertainty

Theme 3: Automation in response to internal turnover

Theme 4: Employee stock purchase plans as a staple equity compensation vehicle

Theme 5: Introduction of ESG reporting to the 10-K and implications for finance functions

But first, let’s cover the Group Five results.

*****

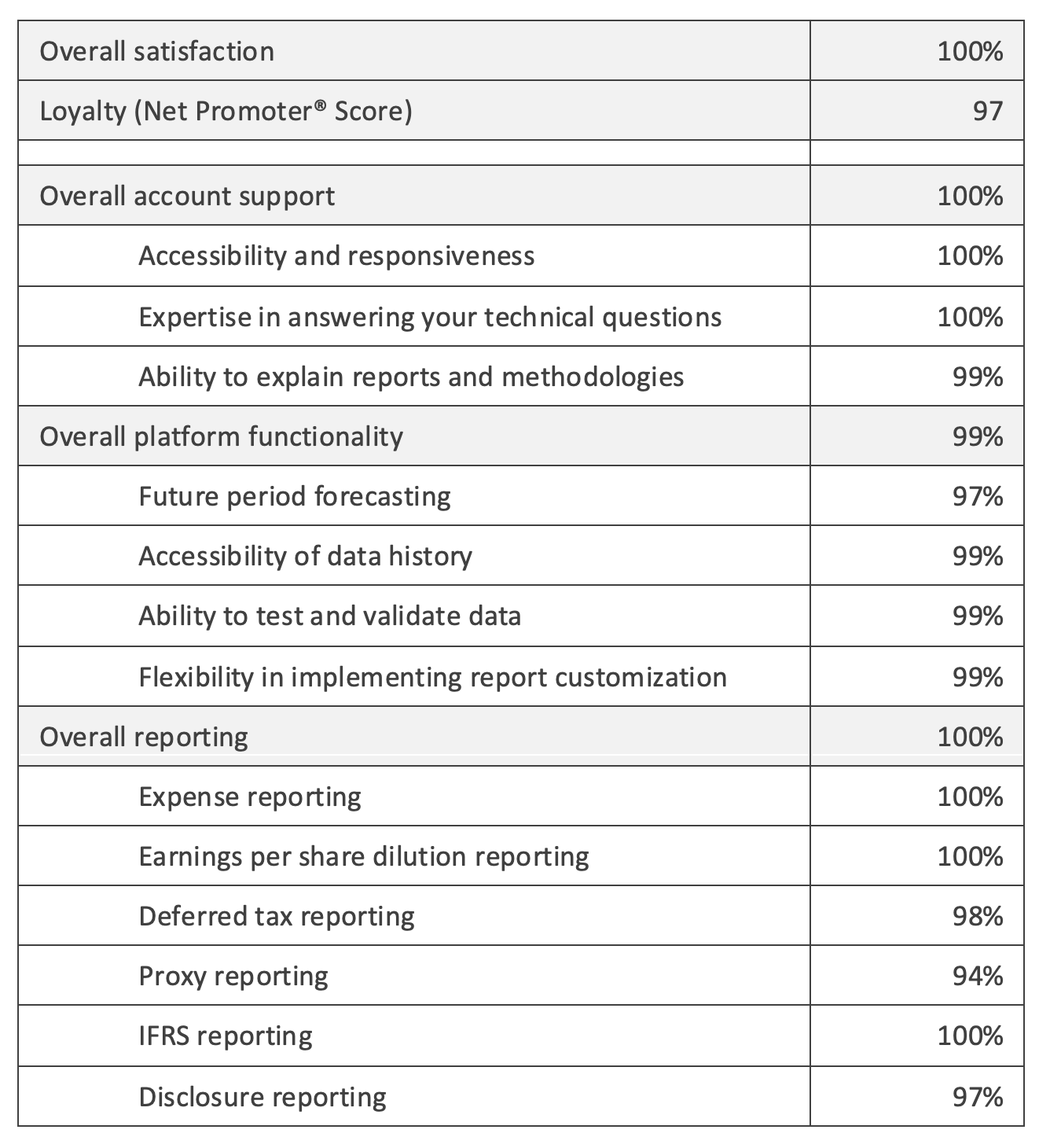

We’re elated to have earned the highest overall satisfaction and loyalty ratings among the financial reporting service providers for eight consecutive years. Group Five uses the Net Promoter Score (NPS) to measure client loyalty. Our NPS is 97 and the industry average is 53:

Here’s a more detailed breakdown of the 2021 results:

2021 has been a tough year for our clients, who are grappling with labor market shocks, hybrid work arrangements, and ever-increasing demands for robust internal and external reporting. It’s such an honor to play a role in our clients’ financial reporting processes for stock-based compensation.

In addition to ever-increasing business as usual reporting, this year we spent a lot of time helping our clients launch and report on new employee stock purchase plans (ESPPs). We also helped them handle the equity in complex acquisitions and spinoffs, implement modifications to outstanding equity awards, and design and account for outsized CEO mega-grants. On top of all that, we worked with our clients to expand the breadth and depth of forecasting in response to heightened market uncertainty.

And that’s just our public company clients (the pubcos, as we endearingly call them). On the non-public side, special purpose acquisition companies (SPACs) made headlines after the SEC retooled the SPAC warrant accounting model this March. And with more companies staying private and wielding greater power in the labor markets, other pre-IPO topics like granting practices and profits interest programs occupied much of our clients’ attention.

It’s always so touching to read the open-ended comments our clients share. Here are a few that really bring home that our “why” is to serve you:

From all of us to all of you, thank you for your recognition. We’re honored to support you.

With that, let’s look at some themes ahead in 2022.

At least in the equity markets, economic catastrophe was averted in 2021 as inflation and government stimulus fueled a precipitous rise in security prices for most companies. But that hasn’t made compensation goal-setting easier as general levels of uncertainty remain at protracted levels. With today’s inflation worries and supply chain disruption, setting earnings three years into the future can feel like a guessing game.

As a result, the adoption of relative performance awards is spiking. In 2020, approximately 57% of the S&P 500 used a relative TSR (rTSR) metric in their long-term incentive plan (LTIP). In 2021, the number climbed to 72%. We expect to see that number exceed 75% in 2022. Relative financial metrics appear in 22% of cases where a financial metric is adopted, with the most common flavors being relative return on capital and relative EBITDA growth.

We’ve covered in many other settings why relative metrics simplify performance goal-setting and focus performance on the factors within management’s control by filtering out macroeconomic noise. Let’s look at some of the implications this trend has for financial reporting leaders.

And for a basic overview on the valuation of awards with market conditions, check out our introduction to Monte Carlo simulation.

Insofar as economic uncertainty and disruption are macro themes for 2021 and the indefinite future, forecasting is one of finance’s most powerful solutions. Scenario-based forecasting helps color the range of future possibilities to set expectations and avoid surprises.

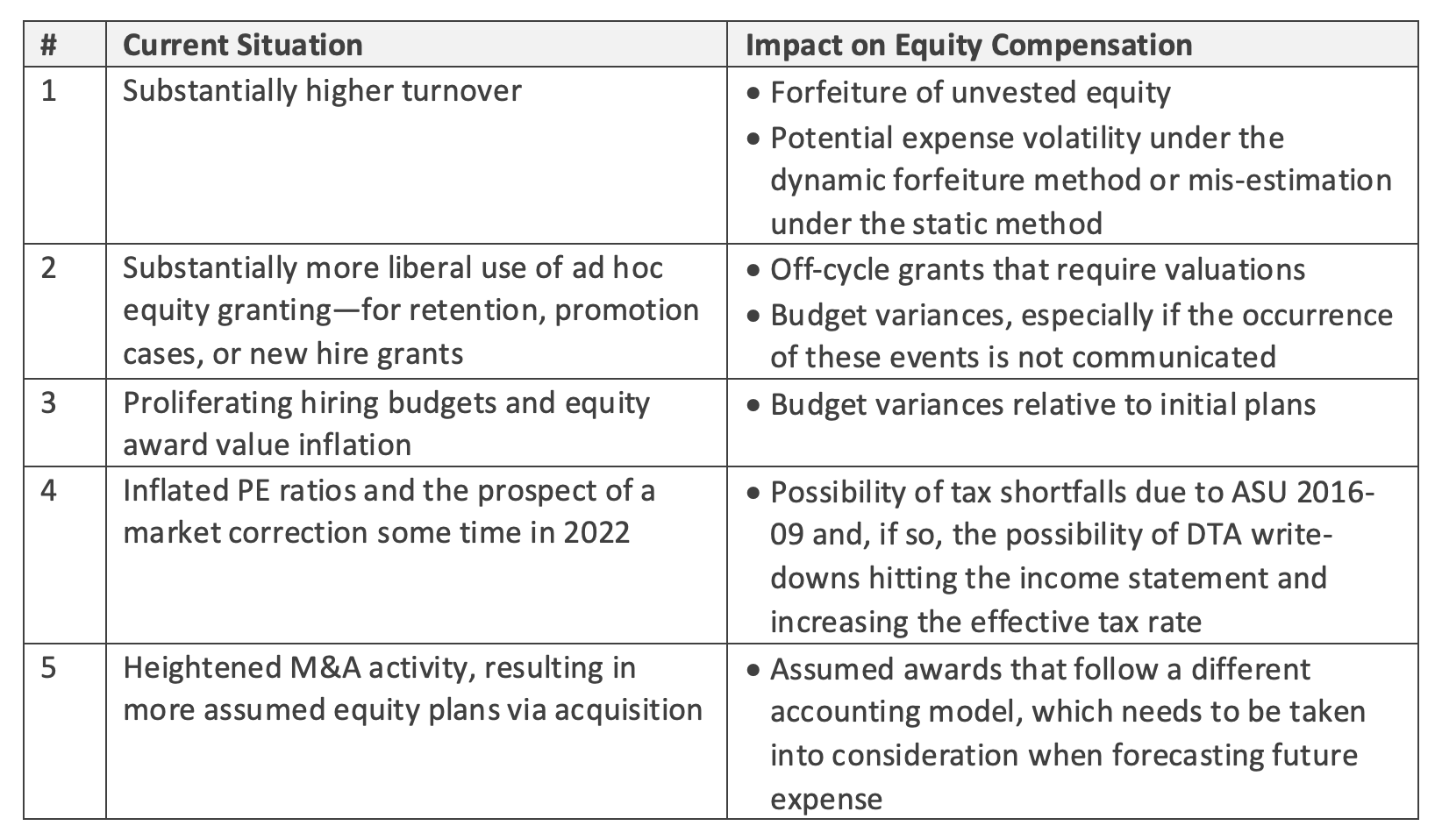

Let’s look at some of the ways in which macroeconomic uncertainty and complexity are specifically impacting stock-based compensation:

We’ve published extensively on forecasting best practices and run a webcast on the same. We’ve also honed in on tax settlement forecasting given ASU 2016-09’s unique effect on the income statement. Here are a few tips and best practices to consider:

We expect the pressure surrounding robust forecasting to tighten given the volatility in both the equity and labor markets. We’re also seeing investors pushing back on non-GAAP earnings metrics that exclude stock-based compensation once firms reach large cap sizes, further prompting a need to understand and model future trends.

Our value proposition has never been one of replacing staff. Rather, it’s about allowing our clients’ staff to shift their focus to higher-value activities—analysis, internal reporting, cross-functional collaboration, or new and emerging accounting standards. But as the Great Resignation has taken hold and no company has been immune, the need for automation couldn’t be higher.

To be sure, automation may involve engaging a third-party organization like ours. Or it could occur internally using technologies like Access or SQL. The answer will in part depend on the complexity, materiality, and availability of internal resources.

Much has been written about the dangers of spreadsheet-based processes. We’ve shared our thoughts as they relate to stock compensation, and there’s no shortage of more general literature touting the benefits of automation.

Rather than restating the benefits of automation, let’s focus on where automation can be most critical in reducing key person risk or manual processing risk. One way to find out is by asking the following questions:

Automation is sort of like cybersecurity: everything is fine until one day when it isn’t. Best-in-class accounting functions will look around the corner to see how needs are evolving so they can get ahead of risks. With so much labor market turmoil and the loss of institutional knowledge, the benefits of automation have grown for many companies in 2021.

ESPPs have made a seismic comeback after dwindling during the adoption of ASC 718 in 2006. ESPPs are cost-effective, incredibly diverse in how they can be structured, and all but certain to be approved when put to a shareholder vote. Employees like them too, if the plan has favorable provisions.

Of course, this is referring to the modernized version of ESPPs, where a 15% discount and lookback feature are just the beginning. We’ve covered ESPP design topics extensively, including in this Workspan article, this blog post on ESPP trends in the tech sector, and this webcast. The more generous the ESPP provisions, the higher the income statement cost—but our experience is that this lets companies shrink their RSU granting and experience large upticks in the perceived value of the equity program.

We’ve seen this trend for a few years, but 2021 was a breakout year for ESPPs. They’re most prevalent in human capital-intensive sectors like technology and life sciences. Even so, we’re seeing companies in other sectors launch ESPPs so they can stand out to talent. In tech and life sciences, a generous ESPP is becoming table stakes.

What does this mean for ESPP financial reporting? A lot. ESPPs are more complex to account for than any other equity vehicle we work with. This is in part due to the numerous provisions and design flexibility. It’s also linked to the scale of ESPP programs, wherein they must be made available to all employees (within a corporate legal entity). The more favorable provisions include modifications that go into effect by sudden moves in the share price or participant elections.

Here are some insights to consider if you’re planning to roll out an ESPP or are coming up to speed on an existing one:

We predict ESPPs will become even more popular. They’re not for every organization, especially where most employees earn too little to set aside part of their paycheck for an ESPP (though multiple fintech companies are trying to solve this problem). However, when it fits the demographics of your employee base, an ESPP can be a key asset in the competition for talent.

Our last topic is the onset of ESG reporting in the 10-K. To date, we’ve focused on the SEC’s human capital management (HCM) 10-K disclosure that went into effect in 2020. This past September, we ran a webcast looking at results from the first year of mandatory disclosure. The webcast built on a report published earlier in the year on these same disclosures.

Our first-hand experience advising companies on this disclosure was extremely varied. Large caps tended to view ESG reporting (in the 10-K or any financial document) as a vehicle for telling a differentiated story in pursuit of alpha (finance parlance for excess returns). Smaller companies tended to view this as a check-the-box exercise. And, as is typical in the first year of any new regulation, there was considerable variation regardless of firm size or industry.

Here’s where it gets interesting and why we think ESG reporting in the 10-K is something to watch. The SEC has stated an intent to modify the existing HCM disclosure and introduce a disclosure requirement on climate-related risks. The HCM revisions are likely to impose specific ratios and calculations given the SEC majority’s opposition to the principles-based approach taken by the prior administration.

ESG-related disclosure is important to different pockets of investors. The passive institutional funds (which represent the vast majority of voting power) have declared that this is the most important issue to them. Activists have conveniently found ESG to be a lightning rod to suit their agendas.

This might sound strange given what all of us learned in school, which is that investors buy and sell in response to earnings—future potential earnings, actual earnings misses, etc. The problem is that passive investors cannot buy and sell in response to quarterly earnings data. Their sole recourse is their proxy vote, where they vote to reject or reelect directors and to reject or accept shareholder proposals. In this regard, the proxy has become a much more important filing than ever before. As one CFO put it to me, “the proxy is the report card for my boss’ boss” (he was referring to the lead independent director who reviews his boss, the CEO).

If more disclosure on human capital and environmental topics is coming down the pike, here are a few things you can do to prepare:

I mentioned earlier that ESG reporting is a differentiator for many large companies and a perfunctory exercise for many smaller companies (with abundant exceptions). We think this will change. Hopefully, earnings and other fundamental financial data will remain the driver of asset values, but we think investors of all shapes and sizes will embrace the opportunity to grade companies in more varied ways. After all, they have nothing to lose by pushing for a more flexible report card.

Now is a good time to begin preparing for the onset of ESG reporting in otherwise traditional financial reporting.

We’re so grateful for the opportunity to serve our clients and deliver best-in-class financial reporting. Our most sincere thanks to our clients who generously gave their time to Group Five’s benchmarking process.

Read the summary report to learn more about this year’s results.

Visit our knowledge center for more on the above topics.

Tell us about any other topics you’d like to see us cover.