Subscribe to Our Newsletter

Hear more from Equity Methods: Your trusted partner in equity compensation excellence.

Each year, our team engages with hundreds of companies and fields thousands of questions, ranging from foundational elements of stock-based compensation to complex, organization-specific challenges. Many of these questions strike a healthy balance of being nuanced enough to spark deeper thinking, yet broad enough to resonate across industries.

That’s the spirit behind the Equity Methods Mailbag. We share real questions from clients and colleagues—refined for clarity, brevity, and anonymity—along with insights we hope are both practical and thought-provoking.

Topics covered: Fractional shares for tax withholding and ESPP purchases, Section 162(m) and the ARPA Five, retirement eligibility and expense acceleration, post-vest holding requirements, pay equity

* * * * * * * *

Transitioning to a fractional-share model for tax withholding and ESPP purchases is a strategic upgrade that enhances both fiscal precision and participant value. By moving away from a whole-share model, companies avoid the need to over-sell or over-withhold shares for tax obligations, which can lead to excess cash remittances and reconciliation issues. Ultimately, fractional shares allow employees to retain more equity while streamlining the internal tax withholding process.

However, there are a few operational watch-outs to consider:

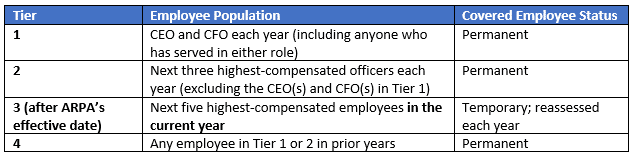

Legislative changes to the deductibility of employee compensation under Section 162(m) have really kept tax and HR departments on their toes. First, we had the Tax Cuts and Jobs Act (TCJA) of 2017, which removed performance-based awards from the deductibility exceptions and made permanent any additions to the covered employee list. Then, in 2021, the American Rescue Plan Act (ARPA) added five temporary employees to the covered list each year, effective for tax years ending after December 31, 2026.

ARPA is more complex than simply identifying the next five highest-compensated officers. While TCJA established “once covered, always covered,” the additional five employees under ARPA are temporary and must be reassessed each year. Further, this new group expands the population beyond officers to include all employees, requiring more robust identification and reporting processes. The table below summarizes the covered employees each year. With this new Tier 3 population, employee tracking becomes much more complex. Atypical compensation like major hiring events, one-off retention grants, or outsized annual bonuses can make the list highly volatile compared to the pre-ARPA framework.

With this new Tier 3 population, employee tracking becomes much more complex. Atypical compensation like major hiring events, one-off retention grants, or outsized annual bonuses can make the list highly volatile compared to the pre-ARPA framework.

Although the ARPA update is effective for tax years ending in 2027 or later, the employees in Tier 3 are already relevant today. Any tranches being amortized now with expected settlement dates after 2026 need to be assessed for deductibility. The question is, who will the rotating ARPA Five be next year, and the year after?

One approach we’re seeing companies take is assigning Tier 3 employees based on the best information available today. That best guess may fluctuate over time until fully locked in by the end of each tax year. This can lead to large adjustments on an employee level as updates are made, with additions and subtractions offsetting to some degree. The emerging best practice is to combine robust tranche-level forecasts with actual settlement activity to predict compensation by employee, then flag each tier using an officer list and track the effective year for Tier 3 employees.

Another approach is to apply an on-top haircut to deferred tax asset balances, which get trued up at year-end once the final list of covered employees is known. Determining the appropriate haircut requires an analysis of its own. And while high-level estimates may lead to larger adjustments later, this haircut method may be easier than forecasting the exact list early in the year.

Naturally, this additional 162(m) complexity is pushing forecasting processes to their limits. We encourage companies to thoughtfully construct assumptions and are happy to share insights from reporting processes we’ve architected. A deeper discussion of how companies are adjusting for the ARPA Five in their current-year balances and forecasts is available in our blog post on the topic.

This is a common question during annual grant season, when many companies review their equity awards in detail to ensure accounting treatments align with legal agreements.

As a refresher, expense for equity awards is amortized over the requisite service period. When an employee becomes entitled to any portion of unvested shares due to a retirement eligibility (RE) provision, that RE date is factored into the requisite service period. If the RE date occurs before the end of the award’s stated vesting schedule, expense is amortized over the shorter period from grant date to RE date.

There are different degrees of retirement eligibility in practice. Full retirement eligibility provisions allow employees to retire at a specified age and/or years of service while retaining all unvested equity (regardless of whether shares are delivered upon retirement or based on the original vesting schedule). With this feature, all expense must be recognized at the earlier of the vesting date or the RE date.

However, there are many variations of RE. Some retirement features create a substantive service period, even after employees meet the RE requirements. The three most common examples of retirement features that come with some portion of expense being amortized after an RE date are:

Beyond the expense impact, RE provisions can also affect diluted earnings per share (EPS). Under ASC 260-10-45-13, shares that are no longer contingently issuable should be added to common shares outstanding when calculating basic EPS. This is applicable to time-based restricted shares without any of the RE restrictions above. On the other hand, stock options and performance awards typically have contingencies even after RE is reached, so no inclusion in basic EPS is needed.

For more information, we have a dedicated retirement eligibility webcast and several related resources in our Knowledge Center.

Post-vest holding requirements—which require executives to continue holding vested shares for a specified period after vesting—have gained a solid foothold in recent years as an important executive compensation tool, especially for larger and more sensitive grants. Some of the key benefits include:

Additionally, post-vest holding requirements on time-vesting awards will now be viewed more favorably by ISS following their updates for the 2026 proxy season. Now, ISS’s qualitative evaluation won’t raise concerns about pay mix due to a lack of performance-based awards, so long as time-vesting awards incorporate at least a five-year time horizon when combining vesting and post-vest holding periods.

That said, there are three main pitfalls we see when implementing a post-vest holding requirement.

First is the recipient pool. Put simply, these requirements can be a good fit for top executives, but not necessarily below that level. Executives have larger overall holdings, fewer liquidity constraints, and are accustomed to trading restrictions. Broader-based recipients are more likely to be (or perceive themselves to be) adversely affected by these restrictions.

Second is the valuation discount. Post-vest holding requirements can qualify for a DLOM, which reflects a discount in fair value due to the restriction on sale. This discount will in turn lower the accounting cost associated with the award, which can result in cost savings or more units granted for the same value.

However, for an award to be eligible for a valuation discount, the restriction must be a feature of the security itself, not specific to the holder. In practice, we see two main pitfalls that can invalidate the DLOM:

It’s important to avoid these pitfalls, or else the restriction will not be independent of the holder’s employment or other holdings, and the DLOM will not apply. To learn more, see our article “Demystifying the DLOM: Discounts for Lack of Marketability for Post-Vest Holding Requirements.”

The third pitfall is tax-related. Post-vest holding requirements should apply only to shares received by the holder net of any shares withheld or sold to cover tax requirements. This avoids creating “dry income,” where a taxable event occurs but the executive has no ability to use the proceeds from that event to pay the associated tax bill. Because the restriction applies only to the net shares received, it’s generally appropriate to apply the DLOM only to the fraction of shares the recipient will hold after taxes.

For many organizations, the annual merit cycle is the most significant pay decision moment of the year. It’s when managers translate performance assessments into pay and promotion decisions. That makes it both a major opportunity and a major risk when it comes to pay equity.

If inequities exist going into the cycle, or if guardrails are weak when annual pay adjustments are determined, the merit process can unintentionally widen pay gaps. On the other hand, the merit cycle can also help proactively close gaps when organizations complete a pay equity assessment immediately beforehand. (For more on this topic, see “Getting the Conversation Started on Pay Equity Remediation.”)

Before the merit cycle. With this in mind, we typically suggest performing a statistical pay equity analysis before the start of a merit cycle. This helps identify structural pay disparities so that any corrective action can be embedded into the review process. Reviewing pay equity before merit decisions are finalized helps ensure compensation outcomes are equitable and aligned with the company’s compensation philosophy.

During the merit cycle. A robust pay equity analysis does more than quantify pay gaps. It also provides insights into how much each factor (such as performance or time in role) impacts pay.

These insights can help managers make more informed and equitable pay decisions. For example, if a company promotes a pay-for-performance culture, but the analysis shows that performance rating is not a significant predictor of pay, that disconnect should be addressed during the merit process.

Additionally, we suggest doing a “refresh” of the analysis based on proposed merit increases. This serves as a final checkpoint to identify emerging disparities before decisions are finalized.

After the merit cycle. Equally important is what happens outside of merit season. Pay gaps can develop through cumulative off-cycle actions like new-hire offers, retention adjustments, and role changes (to learn more, see our article “Maintaining Pay Equity: Analyzing the Impact of New Hire Pay”). Regular pay equity analyses, combined with strong year-round infrastructure around job architecture and compensation frameworks, enable companies to maintain pay equity.

In the US, while there is no federal mandate requiring pay equity analyses, laws like the Equal Pay Act (EPA) and Title VII of the Civil Rights Act make it illegal to pay employees differently based on gender, race, or other protected characteristics. Many states (including California, Illinois, and Massachusetts) have enacted additional pay equity laws.

Companies that conduct regular reviews are better positioned to defend their compensation decisions if challenged and to address potential disparities before they become compliance issues. The EU Pay Transparency Directive introduces even more stringent requirements for companies operating in Europe.

Regular pay equity analyses therefore help companies comply with these requirements, strengthen corporate governance, and signal a commitment to fair, transparent, and defensible compensation practices—reducing both legal and reputational risk.